by: Veronica Cardinale Ellinger, CEO Murphy Business Sales Today’s Market Makes Protecting Your Business’s Value Essential If you are thinking about…

Read More

Murphy Business and Financial Corporation LLC (MBFC), one of North America’s leading business brokerage firms, is proud to announce its…

Read More

by Veronica Cardinale Ellinger, CEO, Murphy Business Sales At the beginning of every New Year, ranking lists that reflect top…

Read More

by Veronica Cardinal Ellinger, CEO of Murphy Business Sales As 2025 draws to a close, a significant trend is clear:…

Read More

When it comes to selling a business, one of the first and most important questions is: What is my business…

Read More

Murphy Business Sales, one of North America’s largest business brokerage and mergers and acquisitions advisory firms, is proud to announce…

Read More

When most people think about business broker qualifications, they picture licenses, certifications, and financial know-how. While those technical skills are…

Read More

The economic headlines of 2025 are hard to ignore. With inflationary pressures, uneven consumer demand, and a cautious lending environment,…

Read More

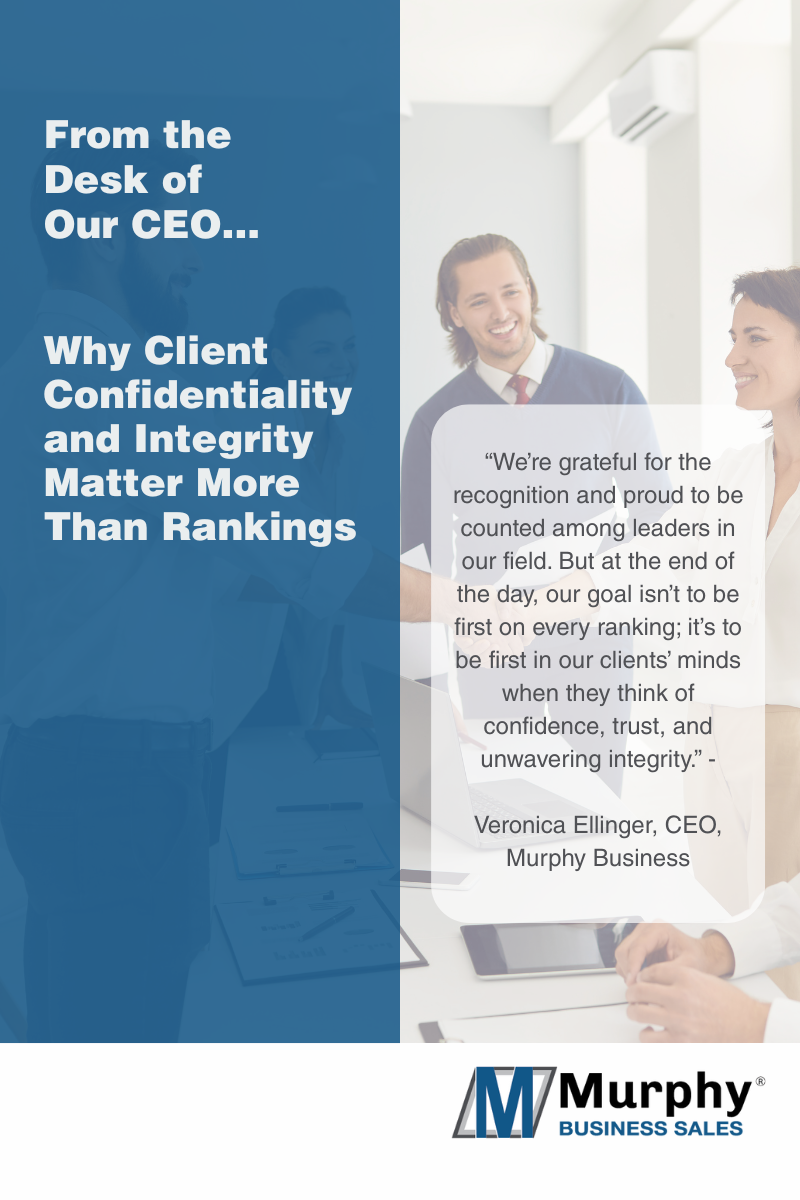

Client Confidentiality and Integrity Come Before Rankings — At Murphy Business Sales, these values guide every decision we make.…

Read More